Fachwissen für den Mittelstand

Der VBU Blog

Lernen Sie unsere Experten und Autoren kennen. Fachwissen für den Mittelstand.2024 - A Challenging Year of the Dragon

Entering the Year of the Dragon, a symbol deeply woven into the fabric of the culture, China encounters the supreme emblem of power, nobility, honor, luck, and success. 2023 presented the Chinese economy with a formidable array of challenges, navigating through turbulent waters encompassing real estate uncertainties, demographic shifts, and the complex dynamics of debt and geopolitics. As China strides into 2024, the crucial question arises: How will this new year shape the nation's economic landscape? Amidst the relentless headwinds and burgeoning challenges, how will the nation confront and adapt in The Year of the Dragon?

The Dragon Challenge

With the reopening of borders and the relaxation of COVID-19 restrictions in early 2023, the primary hurdles for engaging in business with China have undergone a notable shift, as the pandemic no longer takes precedence as the foremost challenge. However, the risk-adjusted return on investment in China is not comparable to its pre-pandemic status. The scope and magnitude of changes in China's business landscape are extensive, influencing decisions for companies on multiple fronts in 2024 and beyond:

Maturing Economy – Slower Growth

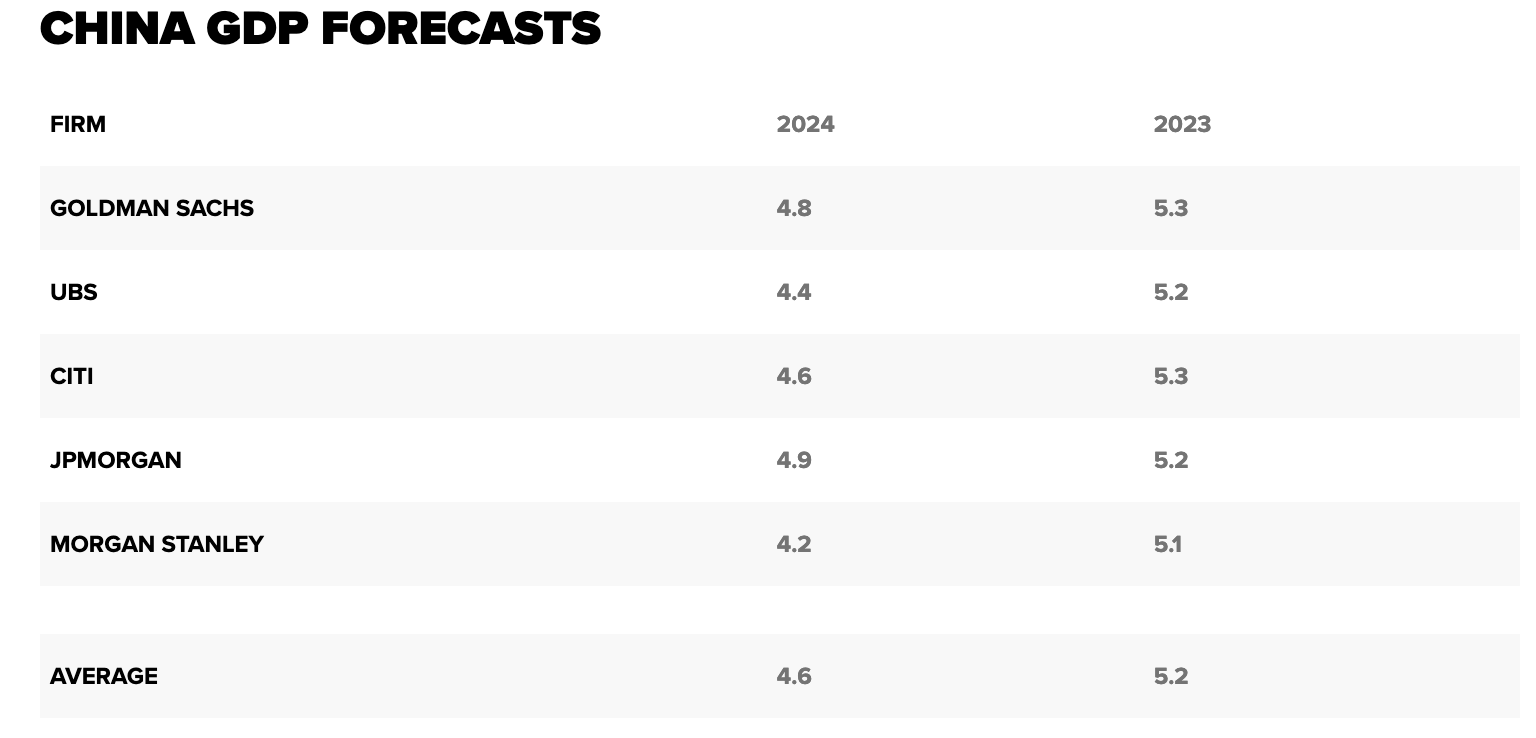

After three decades of double-digit GDP growth, China's economy has experienced an alteration. Between 2011 and 2022, annual GDP growth averaged 6.6 percent, marked by fluctuations intensified by the COVID-19 pandemic. Speaking at the World Economic Forum in Davos, Premier Li Qiang revealed that the Chinese economy grew by approximately 5.2% in 2023. Notably, international investment banks anticipate a deceleration in China's economic growth in 2024 compared to the previous year, as indicated by recent annual forecasts.

(Source: CNBC)

With a projected GDP growth below 5% throughout the rest of the 2020s, Chinese policymakers confront a structural challenge in aligning household and business expectations with a Slower for Longer growth environment (IMF).

In the baseline scenario for 2024, the Chinese leadership will further prioritize national security and domestic stability over economic growth. Policies are poised to emphasize the acceleration of advanced manufacturing capabilities, particularly in strategic technologies, prioritizing the development of vaster domestic capabilities in semiconductors, AI, quantum computing and other emerging technologies.

Geopolitics

In 2024, China faces a challenging geopolitical environment, necessitating efforts from the leadership to stabilize relations with the "West" (particular with the US) for broader foreign policy goals and to instill confidence in China as a reliable partner, crucial for sustaining growth and social stability. The upcoming 2024 US election season, possibly marked by aggressive Anti-China rhetoric, and the EU's growing trade protectionism pose additional challenges to China's ties with the „West“. Moreover, the European Union, a significant investor and trade partner, initiated the de-risking policy approach in 2023 to safeguard its economy without complete economic decoupling. Simultaneously, potential security concerns in the Strait of Taiwan and the South China Sea could exacerbate tensions.

Further Exploration:

U.S.-China Relations in 2024: Managing Competition without Conflict (CSIS)

Meanwhile, various global regions, notably the BRICS nations and Middle Eastern countries, have witnessed a significant uptick in trade and investment with China (however, potential challenges may arise with the BRICS expansion due to Argentina's new president, Javier Milei). These geopolitical changes yield dual impacts. Tensions between China and major western economies directly influence trade and investment, prompting investor caution towards the Chinese market. Conversely, the increasing engagements between China and BRICS and Middle Eastern nations hold the potential to diversify China's trade portfolio, uphold its supply chain significance, and unlock new markets.

Overcapacity – Is A New Trade War Looming?

Rather than steering the post-COVID economy towards domestic consumption, a political choice has redirected capital towards manufacturing, a longstanding pillar of China's growth model. However indicators suggest that relying on investment and manufacturing alone may make it challenging for China to consistently achieve a 4-5% GDP growth.

This shift, channeling financial resources from the ailing real estate sector to manufacturers instead of households, has resulted in industrial overcapacity across important sectors (NEV, renewables, chips, etc.), tending to increased industrial overcapacity and a rise in international trade tensions. In strategic sectors favored by Beijing, China's trading partners may see protective trade measures as essential to safeguard their industrial bases from Chinese overcapacity.

Further Exploration:

China’s structural slowdown augurs more global trade wars (Hinrich Foundation)

Structural Domestic Challenges:

Property Market, Local Government Debt &

Youth Unemployment

Given the substantial contribution of real estate to China's GDP (At its peak, China's residential property sector was thought to contribute an estimated 25%-30% of the country's GDP), implementing effective policies to stabilize the sector remains paramount. In 2024, a key focus is managing the downside risk in the economy, specifically stemming from a correction in the housing market and its potential spillover risks. Preliminary indications suggest that China's January 2024 home sales may underwhelm the market, potentially instigating a bearish outlook for the country's property sector and the broader economy.

Due to the fragility of the housing market, especially in smaller cities, private sector sentiment is constrained by property pessimism. With speculative demand diminishing and existing price controls still in place, the presales model has generated a notable excess supply issue. Resolving this entails addressing the substantial overhang in the sector's existing inventory and reducing the surplus leverage of property developers. The recent Evergrande liquidation and uncertainty regarding measures to support the equity and stock markets contribute to an expanding array of pressing economic challenges.

Further Exploration:

Real Estate Is China’s Biggest Economic Vulnerability (GPF)

China's centralized fiscal system played a pivotal role in the country's economic success over the decades but also contributed to the escalation of off-balance-sheet local government debts. The rising debt burden on local governments presents a potential obstacle to vital investments for economic revitalization, given that historically, local authorities have shouldered around 70% of China's annual state-led infrastructure investment (Oxford Economics).

In 2024, an anticipated shift involves an augmented role for the central government in fiscal expenditure and the nationwide coordination of financial resources. This shift may include transferring specific spending responsibilities from local authorities to the central government, easing local fiscal strains and preventing a resurgence in local borrowing during the ongoing debt clean-up.

China's post-COVID economy hasn't alleviated the challenges in the youth labor market. Despite a surge in fresh graduates, there hasn't been a corresponding increase in new job opportunities. The persistently lower wages offered to new hires reflect the oversupply of labor.

Youth unemployment is expected to persist as an issue in 2024, but may gradually alleviate during the forecast period (2026-28) in combination with a sustained decline in the working-age population. However, until then, the economic struggles caused by youth unemployment will have lasting consequences, including reduced lifetime earnings and purchasing power, along with delayed marriage and childbirth, carrying negative long-term implications for demographics (EIU).

The German Perspective

While Germany maintains a firm stance on political issues, its businesses are increasingly adopting a pragmatic approach on China. The 16th edition of the AHK Business Confidence Survey (conducted between September and October 2023) gathered responses from 566 member companies, providing a highly representative snapshot of German businesses' sentiments in China. Despite a slower-than-expected economic recovery, China remains uniquely significant to the German economy, holding the position of Germany's most crucial trading partner for seven consecutive years.

Approximately 40% of respondents anticipate an improvement in industry development, marking a return to pre-COVID levels. Notably, 90% of German companies foresee China's economic recovery within five years. The commitment to the Chinese market has strengthened, with 91% of surveyed companies expressing dedication, a 2% increase from the previous year. However, cautiousness prevails in investment plans, with only 54% of companies intending to invest in China within the next two years, compared to 67% in 2019.

China's attractiveness stems significantly from its innovation potential, although geopolitical tensions (83%) are the primary reason prompting risk management efforts. In case of operations have to be shifted, other Asian countries emerge as the preferred destination. On the downside, legal uncertainty tops the catalog of regulatory challenges hindering German companies in China, followed by cyber and data security regulations. Moreover, more then half of German companies participating in public procurement still encounter discriminatory measures.

Eating Bitter - 吃苦

In 2024, China confronts a onerous "Year of the Dragon", contending with complex national and international challenges. Despite signs of economic recovery post-COVID, the persistent strain on economic growth remains a constant throughout the year. Geopolitical tensions, imminent trade conflicts, the looming possibility of decoupling, and unresolved structural problems on the domestic front will be central to China's narrative in 2024.

Key concerns include the trajectory of the COVID-affected economy, with top leadership aiming for a comprehensive enhancement in economic activity and a substantial boost in domestic demand. Against the backdrop of global economic uncertainties, questions arise about the efforts of the two powerhouses, the US and China, in stabilizing their political relations and whether a new Trade War will emerge. The revitalization of the property market is another focal point, prompting inquiries into whether there will be a robust strategy to bring it back on track. Additionally, there is a pressing question of whether China can pursue its ambitious technology advancements amid escalating internal regulatory interventions and external containment.

A growing list of economic challenges awaits concrete action from Beijing. In the past, economic technocrats crafted effective plans to tackle China's economic concerns. However, there is now a noticeable absence or discreet action. But: restoring widespread customer and investor confidence remains uncertain until these challenges and unresolved issues are adequately addressed. Consequently, China's economy might face another year of (吃苦) “eating bitter”.

Further Exploration:

Beijing’s Silence is Deafening (Rhodium Group)

Five big uncertainties facing the Chinese economy in 2024 (PIIE)

Dirk Mueller VBU Partner in Shanghai

As a Shanghai-based VBU Partner and seasoned strategy and strategic marketing consultant, the author specializes in guiding small- and medium-sized enterprises to success in China. Leveraging expertise in trend and market analyses, strategic development, project support, intercultural competence, and an on-site China service network, the author empowers businesses on their journey into the Chinese market.

Sources:

EAC INTERNATIONAL CONSULTING: China in 2023, December 2023

Economist Intelligence Unit (EIU): China Outlook 2024

EY: 2024 Geostrategic Outlook, December 2023

German Chamber of Commerce in China: Business Confidence Survey 2023/24

Oxford Economics: Research Briefing China: Key themes 2024 – A slower, but healthier, dragon year, December 2023

Photo: Dirk Mueller

Wenn Sie den Blog abonnieren, senden wir Ihnen eine E-Mail, wenn es neue Updates auf der Website gibt, damit Sie sie nicht verpassen.

Über den Autor

Kontakt

Verbund beratender Unternehmer e.V.

Adenauerallee 12-14

53113 Bonn

Telefon: +49 228 966985-19

E-Mail: vorstand@vbu-berater.de

Kommentare